Cash Flow:

A Statement of Cash Flow organizes the company results in a manner to show what elements brought cash into the company and which activities required cash outlay. Like the Income Statement, it covers a specific period of time.

For companies using purely cash-based accounting, there will be little difference between the Income Statement and the Statement of Cash Flow. Under the accrual-based method, however, timing differences between actual transactions and their cash settlement are held in the Balance Sheet. It is, therefore, logical to extract the sources and uses of Cash by examining period-to-period changes in the Balance Sheet.

A standard presentation of Cash Flow groups the sources and uses of cash by Operating, Investing, and Financing activities.

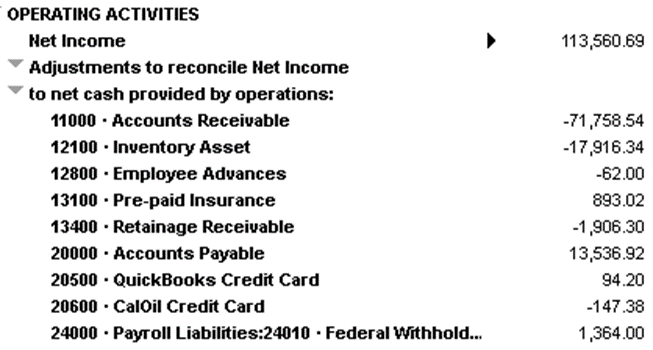

Operating Cash Flow begins with Net Income, and then recognizes the changes in Accounts Receivable, Prepaids, Payables, credit cards balances, and Payroll liabilities:

Investing Cash Flow identifies longer term investment in the company’s future:

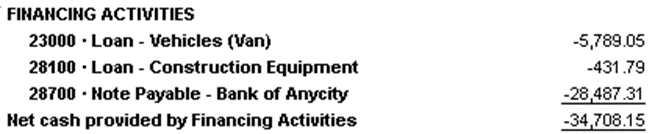

Financing Cash Flow shows outside investment and other methods of financing company operations:

The net result is:

The Statement of Cash Flows is an important part of the basic financial statements because it aids the business owner in seeing how their daily business decisions impact the Cash balance. These decisions include selling terms, buying terms, use of credit cards or other short-term debt, and the purchase of assets to support the business. Effective cash management can be the key to launching and sustaining a successful business.